Today it is easier than ever to know your FICO credit score. This is the credit score that pretty much all lending institutions look at when deciding whether to provide credit or a loan to someone and how much interest to charge. Your FICO credit score can have a range of 300 to 850. Each bank has its own lending standards but you generally want a credit score of at least 700 to be considered a person with “good” credit and you generally need a credit score of 760 or higher to have “excellent” credit and have a chance to receive the best pricing on loans and credit cards. Data from 2019 shows the average FICO score is a little above 700 and only about 20% of individuals have a credit score of 800 or higher.

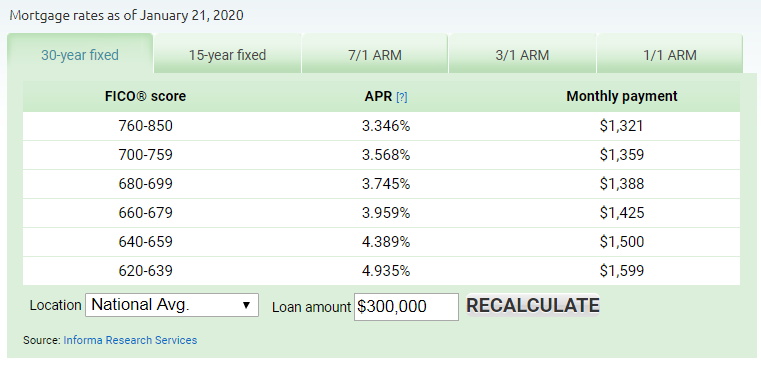

Lenders look at other things such as your income, debt and debt-to-income ratios to determine if you qualify for a loan and the exact terms they will offer. However, having an excellent credit score is the initial threshold you need to meet to have a chance to qualify for the best loan pricing. Your credit score will ultimately impact your interest rate and the amount of interest you will be charged on your credit cards, mortgages, car loans, and student loans. myFICO.com has an excellent calculator to show the differences in the interest rate and monthly payment for different types of loans based on your credit score. Using the calculator, on a $300,000 home loan, you can see how the interest rate and monthly payment on a home loan differs based on credit score.

In this example, assuming you make that monthly payment over the full 30 years, a person with excellent credit (score of 760 or higher) will pay about $100,000 less in interest than the person with a credit score in the low 600s. That is big savings that the person with excellent credit can invest over time.

I have reaped the benefits of having excellent credit

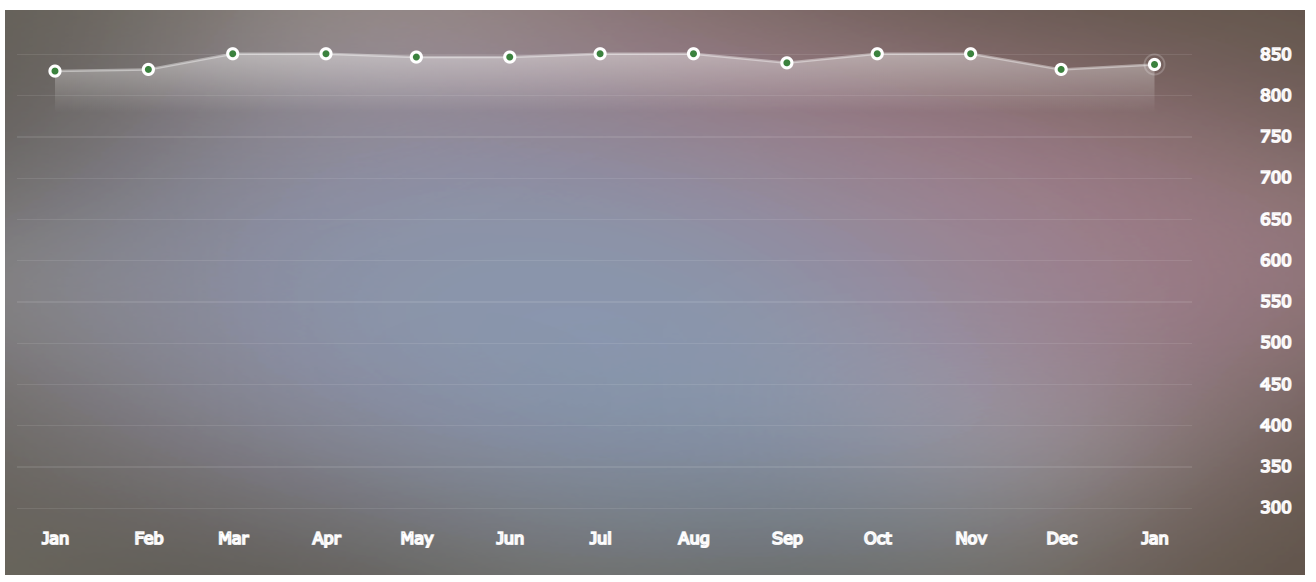

Below is my credit score over the past 12 months.

It is above 800 and has been for a while. I speak from experience when it comes to improving your credit score and how much it matters. Here are some ways my credit score has helped me along the way to achieving financial independence:

- Except for my first home, I have always received the best rates possible on my real estate loans. This has saved me tens of thousands of dollars in interest.

- I have several credit cards with significant available credit because I am considered a low-risk creditor because of my credit history and credit score. I always get the lowest interest rates and I have gotten zero percent introductory rates because of my credit score.

- With two of my real estate investments my partners needed me to be on the loan because they had bad credit. I was able to improve my investment terms between my partners and me because I was taking on more risk and the needed me to get the financing to fund the investments.

The Six Steps to Getting “Excellent” Credit

I’ve outlined seven steps to follow to get a “good” or “excellent” credit score. Assuming you do not have some significant stains on you credit history such as a bankruptcy, following these steps should significantly improve your credit score in just a few years.

Step 1: Know Your Credit Score and Understand Any Issues with Your Credit History

If you do not know your credit score then go find out and see if you need to make any changes to how you deal with credit. Most banks allow you to receive a monthly online update after logging on to their banking platform. You can also get a free credit score from a bunch of online resources. Get a full credit report once per year and understand what is impacting your credit score. Then check your credit score monthly. Do these two things to understand how things are going and so you do not have any surprises the next time you try to get a loan.

I spend five minutes checking my score every month to make sure nothing unusual is happening with my credit score and my credit activity. Five minutes, once per month, it is pretty easy to take this step.

Step 2: Start Building that Credit History

The age of your oldest credit card and the average age of all you credit accounts account for 15% of your total credit score. So get that first credit card as soon as you can but use it sparingly. A person can get a credit card as soon as they are 18 years old. I got my first credit card during college and I used it to buy books, food, etc. Assuming your young self can be responsible with credit, it is a good idea to get that credit card at an early age and start building that credit history.

Step 3: Make Your Payments on Time

Your payment history determines 35% of your credit score. So pay your loans and credit cards on time. It is probably the easiest thing to do to improve your credit score. I always recommend paying your credit cards in full because the interest rates on credit cards are outrageous but if you cannot pay your monthly balance in full at least make the minimum monthly payment so your credit is not impacted.

I missed some credit card payments when I was in college and it was a mistake. All I had to do was make the minimum payment but I was apparently too busy. These late payments impacted my credit score for several years and it cost me a higher interest rate on my first home. Late payments can stay on your credit report for as long as seven years but the negative impact on your score from a late payment does decrease over time if you continue to do everything else right regarding your credit.

Step 4: Keep your Credit Balances Low

Your debt level accounts for 30% of your credit score. The total amount of debt you have and your credit utilization ratio are two major factors that impact this part of your credit score. Credit utilization is the ratio of your credit card balances to your credit limit. For example, if you carry an average credit card balance of $1,000 and you have available credit on your credit cards of $5,000, then your credit utilization would be 20%. The lower your credit utilization ratio the better your credit score. I always try to pay-off my credit cards in full which means I usually have a credit utilization ratio of 0%.

To improve my chances of having a low credit utilization ratio, I periodically call my credit card companies and ask for a larger line of available credit on my credit cards. In the example above, if I increase my available credit on my credit cards from $5,000 to $10,000 but keep the same credit card balance of $1,000 then my credit utilization goes down to 10% just by virtue of increasing my available credit. I suggest building at least 12 months of positive credit history with your credit cards before asking the credit company for an increase in your available credit but it’s worth doing every year or two.

Step 5: Do not Apply for a Lot of Credit at the Same Time

Every time you apply for a credit card or some other form of credit the lender will get a credit check on you. Inquiries on your credit make up 10% of your credit score and the less credit inquiries the better. A few (meaning two or less) will not have a significant impact on this part of your credit score and only inquiries made within a 12-month period have any impact on your credit score.

I recently refinanced the loan on my rental property and my credit score went down about 10 points because of the credit inquiry by the lender. In the chart above you can see the dip in my credit score from the inquiry in December but you can also see how my credit score has already started to recover.

Just be smart with this step. As an example, if you are planning to buy a home and use a mortgage then you should not go and open up a new credit card or other line of credit before your loan application has been approved by the lender. You might also want to make sure potential lenders only perform a “soft” inquiry, which does not affect your credit score, until you decide to proceed with the loan.

Step 6: At Some Point Get that Car or Home Loan to Diversify Your Credit

Credit scores differentiate between two major types of credit – revolving credit and installment loans. Your credit card is revolving credit while things like your home, car and student loans are installment loans. The type of credit you have determines 10% of your credit score so when the time is right (meaning you are going to make a purchase that can use an installment loan) get a loan to diversify your credit history. I used a loan to purchase my second car at age 23 but I also paid-it-off early. I also got my first loan to purchase a home at age 25 and I paid-it-off in full a few years later when I sold the property. These early purchases provided me with a more diversified credit history and by the time I bought my next property at age 28 I had “excellent” credit.

Leave a Reply