If you have been following the economy you are probably asking yourself why it would be time to start buying bank stocks. This sector has been in the toilet since this pandemic started and has not recovered like many other industries.

It’s Been Ugly for Bank Stocks!

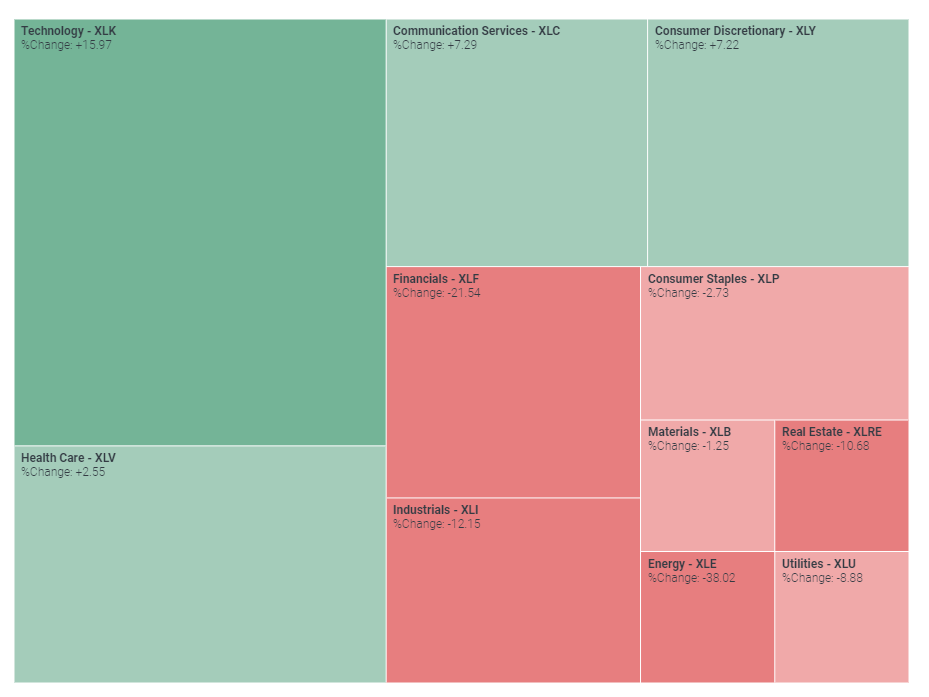

Here is how some large sector ETFs have performed year-to-date:

The financial sector is still 21% down for the year lagging only energy stocks which everyone knows has been a nightmare with oil futures going negative earlier in the year.

Since March I have been buying technology, telecommunication, and healthcare stocks.

I have also been buying real estate and energy stocks over the past few months.

Except for a brief romance with Wells Fargo, I have not owned any financial stocks since April and the ones I held earlier in the year were short term trades. Since COVID-19 reached our shores there has been good reason to be wary of the bank stocks:

- The COVID-19 impact and what state and local governments are doing to combat the virus make it a no brainer that rising defaults and bank losses are going to keep going up in 2020 and perhaps 2021.

- Some business are in the process of getting hammered and will not be able to pay their loans –hotels, other forms of hospitality, retail and restaurant business sectors are going to see some significant levels of defaults on loans and leases. Loans supporting businesses in the energy sector are also going to become suspect with a few sizable players already seeking protection in bankruptcy. Defaults on loans mean banks have to write-down or write-off assets on their balance sheet.

- In fact, since the first quarter banks have been adding significant reserves in anticipation of upcoming defaults. All the banks that hold loans in these challenged sectors of the economy will see some sizable write-offs.

- The Federal Reserve has also promised to keep interest rates low through 2022 to help businesses that are struggling continue to benefit from cheap money. However, a low interest rate environment makes it harder for banks to generate investment income off the spread between the interest rate they charge borrowers and their cost of capital. This means earnings growth will be more challenging for banks as one of their profit generators will become squeezed for the next several years.

- The Federal Reserve is also keeping a close eye on the banks and their balance sheets and most banks have stopped shareholder friendly activities such as stock buybacks. A few banks have also reduced their dividend payments. The Federal Reserve is actually placing restrictions on these shareholder friendly tools.

Why Buy Bank Stocks Now?

Based on the above, bank stocks like a bad investment, right? Well, yes, and that is why the sector is still down more than 20% this year. However, here is why I am going to dip my toe into the financial waters:

- It’s not as bad as originally predicted: A leading real-estate analytics firm analyzed 13,000 commercial mortgages and said cumulative default rate across commercial mortgages will increase to 6.5%, up from the current 0.5% default rate. That’s a big number but the firm noted its current forecast isn’t as severe as its March estimates that predicted significantly higher cumulative default rates in the commercial sector. As an example, in March, the firm wrote hospitality default rates would reach nearly 35% and 16% of retail businesses would default on their loans. The updated forecast reduced default projections to 21% of hospitality entities and only 9% of retail.

- Progress on the vaccine front: With multiple pharma companies feeling bullish on their vaccine prospects I think we need to start factoring in a vaccine approval late this year or early next year which means even the pummeled sectors will start to see a rebound in stock prices and economic prospects. If we get a positive outcome here then people will start getting back to normal with their activities (I think the reopening efforts have shown people are ready to get out and get back to normal life) and when they do businesses will start to generate profits and default rates will slow.

- A lot of quality banks are turning in better-than-expected second quarter results: Make no mistake about it, banks that have reported second-quarter 2020 results so far have recorded significantly higher loss provisions and lower interest rates have affected earnings growth to an extent. However, a lot of banks, such as Goldman Sachs, JP Morgan, Bank of America, to name a few, have beat earnings estimates. Some of these banks have signaled this recession may last deep into 2022 but others have signaled optimism regarding consumer spending and other metrics they can measure based on their loan portfolio and client base. Many banks added significant reserves this quarter assuming a recession that lasts through 2022 to cover upcoming defaults. However, most banks had decent earnings for the quarter even with the loan provisions. Dividends also looked safe for the higher quality institutions absent a total meltdown in the economy later this year.

- Price-to-book values for quality banking institutions are at really low levels: The banking sector in general is trading at book values comparable to the lows of the prior decade despite easily passing the recent Federal Reserve stress tests. As an example, Bank of America is currently trading at 1.2 times book value while it traded near 2 times book value before March 2020. Other companies, like Citigroup and Wells Fargo, are trading significantly below book value. These low price-to-book value ratios have not been since 2016 and more normal ratios should lead to rapid price appreciation after this recession passes.

- The banks are easily passing the Federal Reserve Stress Test: Every financial institution in the Federal Reserve’s 2020 Stress Test passed. In addition to its normal stress test, the Federal Reserve conducted a sensitivity analysis to assess the strength of banks under three hypothetical scenarios due to the current COVID-19 crisis: V-shaped recession and recovery; a slower U-shaped recession and recovery; and a W-shaped double-dip recession. Each bank tested also passed this sensitivity analysis. The Federal Reserve took some measures, like stopping buybacks and capping dividends, but at some point these restrictions will be lifted and banks will again be able to use these tools to deliver value to shareholders.

So how am I playing the Financial Sector?

I am a conservative guy so I am placing three bets:

- I just purchased a closed end fund managed by Blackrock – BlackRock’s Enhanced Equity Dividend Trust (ticker symbol BDJ). The fund’s primary investment objective is to provide current income and current gains, with a secondary investment objective of long-term capital appreciation. The fund invests in common stocks that pay dividends and have the potential for capital appreciation and by utilizing an option writing strategy to enhance distributions paid to the funds holders. It is 26% weighted in financials (it’s largest sector) and its largest holdings include Bank of America, Citigroup, and Morgan Stanley. It is trading at an 11% discount to its net asset value (typically trades at a small 5% discount) and it pays a monthly distribution that equates to an 8% annual yield. This fund gives me exposure to the financial sector, gets me access to some quality assets at a discount, and pays me a solid monthly distribution until I wait for the financial sector to recover.

- I am selling some put options on certain banks in the event third quarter results for the banks are bad. Using put options I can buy these banks at a lower price in October or collect some cash if banks are at their low point and do not go down further. I am selling these put options about 10% below today’s prices with exercise dates in October after the banks report. If the banks stop adding bad loan reserves and have decent third quarter results then I will just collect the premium. If third quarter results look worse than expected, I will pick up these bank stocks at a price lower than if I were to purchase them today. I want to hold these stocks for at least the next several years to see a recovery so I will be happy if I can buy these stocks at prices 10% below today’s level.

- Finally, I am selling put options of financial sector ETFs that are levered 2 to 3 times at exercise prices that are near the March lows for these securities. I get some significant premium with these ETFs because they are levered and volatility remains fairly high in the options market and I will be happy to own these ETFs if for some reason we retest March lows. I am selling these options through my retirement account so I do not have to pay taxes on the premiums I collect from selling the put options. The premiums on these conservative options are providing me with a 10-15% return on my cash if the options expire worthless. Pretty good for a conservative approach.

You need to do your own research but take a look at the financial sector and think about whether you want to add some positions from this sector to your portfolio. It might be time to dabble in this sector.

Leave a Reply