“Everyone has a plan until they get punched in the face.”

-Mike Tyson

As I’ve discussed before, my wife and I want to have our cash flow, or passive income, from investments exceed our annual expenses before my wife stops working and we declare long-term financial independence. Our goal is to obtain annual passive income in excess of $100,000 before the kids go to college. We hope to achieve this goal by 2028. Our goal for 2020 was to achieve $65,000 in passive income.

For the first two months of 2020 things were going according to plan. Here was our passive income goal by investment at the start of the quarter (January 1, 2020):

2020 Passive Income Goal | Investment |

$60,000 | I have an “All Weather Portfolio” in place through my financial advisor that generates monthly distributions. |

$3,000 | I was beginning to create a dividend portfolio to give myself greater exposure to the equity markets but through companies that paid consistent dividends. |

$2,000 | I directly own a rental property that is cash flow positive but not by much. The goal with this asset is to pay down the existing loan over the next few years. |

$500 | I put excess money into a high-yield savings account to round out my portfolio of cash yielding investments. |

$65,500 | Total |

In February 2020, I wrote about how COVID-19 could be a risk to a person’s investments. Since then the major indices for the stock market have gone down by more than 25% from their mid-February highs and volatility in the stock and bond markets are the highest they have been in over a decade.

In March, I significantly re-allocated my investments to reduce downside risk and to be ready to invest in opportunities caused by this current COVID-19 economic downturn. Here are the major changes I made during the first quarter:

- I re-allocated a significant amount of my All-Weather Portfolio, first to gold, and then to cash. I am currently holding about 25% in cash, 30% in real estate debt securities, and 25% in conservative real estate equity funds. The remainder is held in bond and alternative investment funds. I currently have very little exposure to the stock market in this portfolio.

- I increased the amount of cash in my Dividend Portfolio by transferring cash from my All-Weather Portfolio and my high-yield savings account to my Dividend Portfolio. I have invested about 30% of my Dividend Portfolio balance during down days in the stock market but I am holding about 70% of my Dividend Portfolio value in the form of cash. I am actively investing in certain stocks as the market goes down.

- I am in the process of refinancing my rental property to reduce the mortgage interest rate. I am also pulling out a small amount of cash from equity in the rental property to have for future investment opportunities.

- I invested in two real estate crowdfunding projects before the March meltdown with the expectations these investments would cash flow in 2020. I currently do not expect any cash distributions from these investments in 2020 and instead believe cash distributions from these investments should begin sometime in 2021.

I did not expect to take most of these actions when the year started.

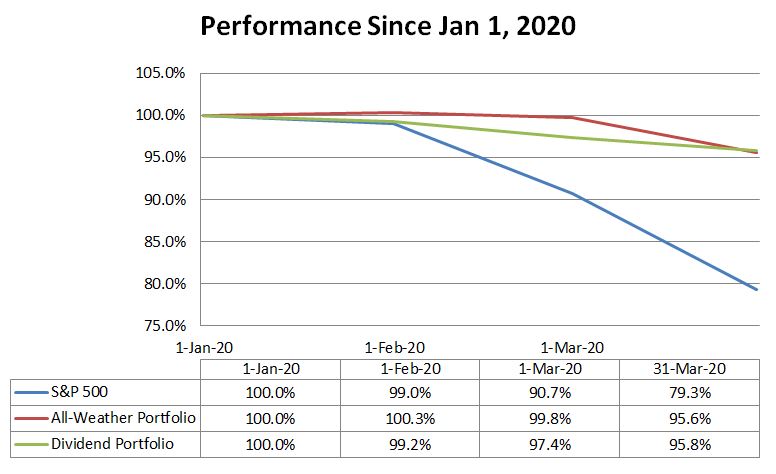

Investment Performance YTD (Through Q1-2020)

Here is the performance year-to-date with my All-Weather Portfolio and my Dividend Portfolio since the beginning of the year as compared to the performance of the S&P 500:

All-Weather Portfolio: My All-Weather Portfolio held up well and did not see a significant decline in market value. To me, this was a big win. My advisor is now looking for more opportunities to invest in the stock market. He is basing his investment decisions based on a U-shaped recession. See here for types of recessions.

Dividend Portfolio: My dividend portfolio has seen mixed results since the downturn. I took too many unnecessary risks by buying some airline and cruise line stocks too early which impacted the performance of my dividend portfolio. I would be up for the year without these mistakes. I am learning from these mistakes though and my investment plan is in place to build a solid dividend portfolio over the next few quarters. I am basing my investment decisions with this portfolio based on a V-shaped recession.

Rental Property: So far my tenant is paying rent but who knows if that will continue. I am hoping for the rent on my rental property to continue to be paid but I would not be surprised to see the rent checks to stop coming in at some point.

Real-estate crowdfunding: I am pretty excited about this new way of investing in real estate but I do not expect to see any cash flow from these investments in 2020 due to the challenging environment for anyone that expects to collect rents right now. The sponsor for my first investment, a multi-family apartment in North Carolina, has already said distributions on all of its properties are suspended until further notice and the sponsor for my second investment, an office property in Washington D.C., would be prudent to build cash reserves until things get back to a more normal economic environment.

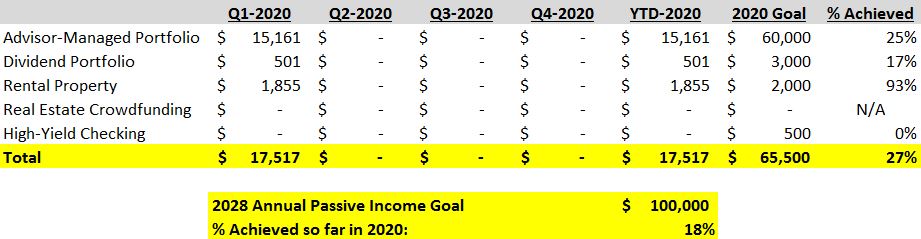

Cash Flow YTD (Through Q1-2020)

Regarding cash flow, after the first quarter we are on pace to achieve our overall 2020 cash flow goal. However, I do not expect to meet our cash flow goal in 2020 because we have shifted a greater percentage of our investment portfolio to cash. The cash we now hold was raised by selling some of the investments that were generating passive income for the portfolio. As we re-deploy the cash into new investments I hope to see our cash flow get back to normal levels. We will begin to re-allocate our cash over time into investments that are being offered at possible discounts. Here are our cash flow figures for the Q1-2020:

Use of Portfolio Income

Another win for my family’s investment portfolio is that we did not have to use any of our portfolio income to pay for our expenses. My wife actually changed jobs and received a salary increase and my part-time teaching job has been a nice source of additional income to cover unexpected expenses. I hope that this positive trend will continue in 2020. We now plan to use our portfolio income in 2020 to rebuild the cash in our high-yield checking accounts.

Revised Expectations for 2020

The 2020 plan going into the year was to increase quarterly cash flow by slowly re-allocating portfolio income to higher-yielding investments. COVID-19 threw this plan out the window.

The revised 2020 plan is to preserve our investment portfolio balance (we did this in the first quarter) and to judiciously re-allocate our increased cash holdings into assets that will be on sale in 2020/2021 due to the COVID-19 economic downturn. The plan is no longer about managing 2020 cash flow on existing investments.

I expect all types of assets to be on sale later in the year, starting with publicly-traded stocks but eventually including debt investments, real estate, and even small businesses.

Leave a Reply