I owe a lot of my net worth to real estate.

I purchased my first home in 2002 and sold it a few years later for sales price 50% above my purchase price. I made over a 600% return on my down payment and this profit allowed me to invest in other assets at an accelerated pace. I paid no taxes on this transaction because the home was my principal residence.

I purchased a Real-Estate Owned Bank property coming out of the Great Financial Crisis and again solid it for 40% above my purchase price a few years later. The return on cash was much greater than 40%. Again, I paid no taxes on this transaction because the home was my principal residence.

I invested in a dilapidated gas station where one of the key parts of the transaction was that we were buying the underlying real estate in a very good area with significant foot traffic. My partners bought me out a few years after I invested. I earned just below 100% on my investment.

I have held real estate mortgages that have provided me a stable 10% dividend yield. I have used these distributions to invest in more assets.

Today, I directly own some real estate as an investment and I also invest in private real estate funds to generate consistent cash flow and some appreciation.

One form of real estate investments that I have not used in the past to generate wealth is publicly-traded real estate investment trusts (commonly referred to as REITs). As we have discussed before, REITs are companies that invest in real estate properties and that are obligated to pay at least 90% of their net income in dividends to shareholders. Most REITs specialize in a certain type of real estate or a specific geographic area. There are good and bad REIT companies just like there are good and bad companies in any industry or sector so you need to do your due diligence on them.

In 2020, when REITs went on sale, I made a good sized investment into a series of REIT stocks. Many REIT stocks have recovered somewhat from their March 2020 lows but most have not recovered fully and some are still trading at a meaningful discount to their 52 week highs.

I am still an active buyer of certain REIT stocks on market dips and I would recommend thinking about adding some REIT stocks (and if your due diligence supports it then consider doing it soon before a vaccine is approved) to your portfolio. Blow explains why I am using REIT stocks as a form of real estate to generate wealth for me in this current environment.

Why I love REIT stocks as investments right now:

REITs have historically been strong performers

The performance of REIT stocks have beaten other stocks over the long-term. One recent study compared the performance of worldwide financial assets since 1960 and found that real-estate investment companies and trusts have beaten inflation by an average of 6.43% a year, compared to 5.45% a year for stocks. Over a 20 year period that means your assets could be 20% greater (more with compounding) if you invested in real estate versus stocks. I know everyone is a tech investor right now but everyone was a tech investor in the late 1990s and those investors took over a decade to recover their losses from the popping of the great dot.com bubble.

Importantly, the study also found that real estate outperforms stocks during recessions and economic expansions and during periods of rising inflation and falling inflation. In this current environment where we don’t know what we are going to see in terms of a recovery and inflation versus deflation you want to own assets that can perform well in different environments.

Today, many REITs are still significantly undervalued despite improving fundamentals

Investors that bought REIT stocks in March are smiling like most investors that invested in other industries. Many REITs have seen 50-100% gains since late March. However, the major U.S. REIT index is still 20% below its February 2020 highs. As we know, the S&P and Nasdaq are much closer to their February 2020 highs and until recently had exceeded those highs. REITs are still trading at a discount due to uncertainty around the timing of an economic recovery and, in some instances, how some real estate asset classes like offices will perform post-Covid. I believe the fears are overdone just as they were overdone for REITs during the financial crisis of 2008-2009.

Don’t take my amateur view as gospel but look at what the pros have been doing. Large asset managers with mandates to invest in real estate have been investing in public REITs inside their private equity funds. These fund managers did this in 2009, made a killing, and they have been doing it in 2020 buying real estate through REIT purchases at discounted prices that are not available in the private market. For example, Blackstone Group, Starwood Capital Group and Oaktree Capital Management made large purchase of public REITs during the first quarter of 2020 even though they traditionally buy real estate through private investments.

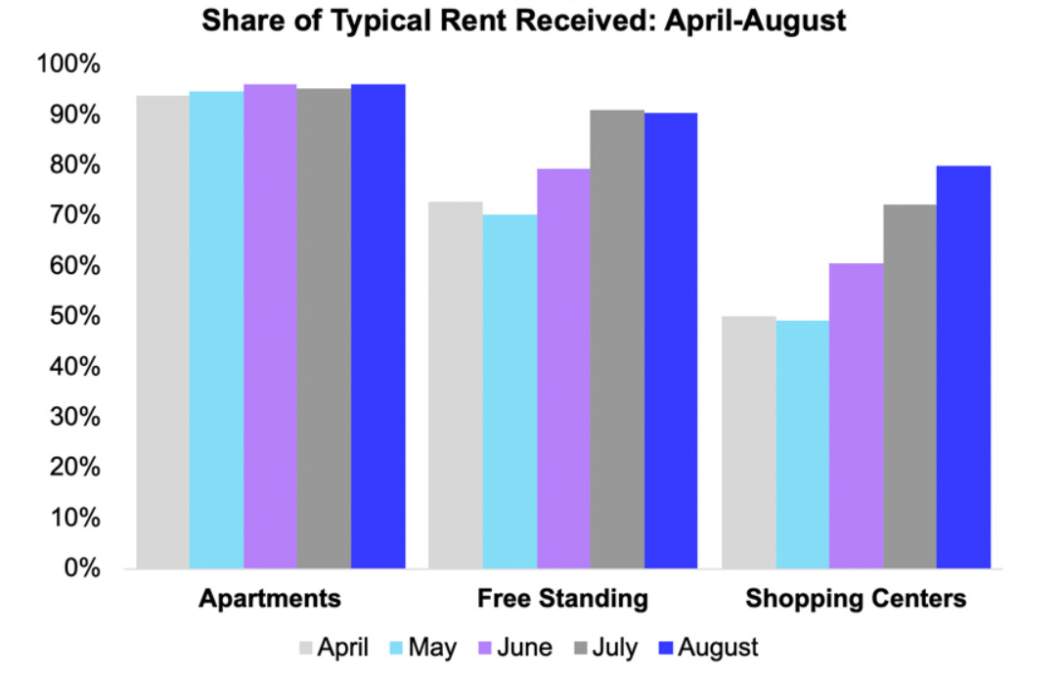

Real estate fundamentals are already improving in many sectors but the public markets are still apprehensive. Take a look at the chart below from NAREIT that shows rent collection rates for apartments, free standing commercial buildings, and shopping centers. Average apartment rent collection rates have remained above 90% throughout the pandemic. Rent collections on free standing buildings are improving and again almost above 90%. Even shopping centers, some of the hardest hit real estate properties which saw average rent collections drop to around 50% in April and May, are now seeing average rent collections exceed 80% in August.

I am not telling you to go find the cheapest REIT stocks and pile in. There is still risk if vaccine candidates fail, new outbreaks of the virus occur in the fall, or a new administration takes a much less economically friendly approach to managing the virus, but those REITs that are undervalued, seeing green shoots of business recovery, with good balance sheets, should be stellar performers over the next 12-24 months.

Yields will become more important over the next few years – the spread between REIT dividend yields and other asset class yields has never been this big

The spread between the REIT annual dividend yield and the 10 year Treasury yield has averaged 130 basis points, or 1.3%, over the long run. However, as of the end of August the spread between these two asset types was greater than 320 basis points, or 3.2%! That is gigantic! Also, remember, the REIT stocks have a history of increasing their dividends over time and many REIT stocks that temporarily reduced or suspended dividends are likely to reinstate dividends now that economic performance for them is improving. REITs in general have a chance to see their prices increase by greater than 50% if the spread between these two asset types return to historical norms and some REIT stocks will see a much greater increase in their stock price if/when this happens.

There is always a chance yields on 10 year Treasury bonds could pop over the next few years which would reduce the spread without REIT stocks going up but I tend to think this is a lower risk scenario over the next few years. Although the Fed Funds Rate and the yield on the 10-year Treasury bond are independent of one another the Fed has already strongly signaled a low interest rate environment for the next 2-3 years. Yield starved investors will find the yields on REITs increasingly enticing during this time.

High quality REITs are in good shape to weather the pandemic and take advantage of opportunities

Back in 2008-2009, the biggest concern of the REIT market was balance sheets. This time around, balance sheets are much stronger. REITs entered 2020 with historically strong balance sheets. Figures shown by other websites show that debt as a percent of the market value of assets accounts for less than 32% of the REITs’ capital stack, down from an average of roughly 45% in the pre-recession period. EBITDA coverage ratios ticked higher to over 5x entering 2020 compared to the sub-3x average in the pre-crisis period.

REIT companies with strong management have also prepared their companies to handle something like the pandemic through restructuring of their debt. The better REIT companies have staggered debt maturities and many of these companies have little to no debt coming due in 2020. Also, many of those REITs have been able to refinance their debt at historically low interest rates. In some instances cash flows are improving because debt that was held at 4-5% interest rates is getting refinanced with new debt at 2-3% interest rates. That’s millions of dollars in reduced interest rate payments for some of these REITs.

The main concern for REITs in 2020 has been the unusually low rent collection rates during the heart of the pandemic. However, as we discussed above, the perception of no one paying rent does not match the reality of what these REITs are seeing with their portfolios. Rent collection rates are improving as the economy continues to reopen and at some point rent collections will get back to normal. I believe rent collections will get back to normal levels by mid-2021. I have no problem investing in REITs, collecting my dividends, and waiting for stock appreciation to occur sometime in 2021, 2022, or earlier.

Some REIT sectors are scarier to invest in – namely malls, hotels, and office space. However, other sectors, such as triple-net, grocery store anchored shopping centers, and apartments, should not invoke much fear into investors and are still trading at discounts. There is potential reward by investing in malls, hotels, and office space – and I will be writing an article soon on how I am doing this – but even the more secure plays still have some potential.

REITs will pay nice dividends while I wait for their stock prices to rebound

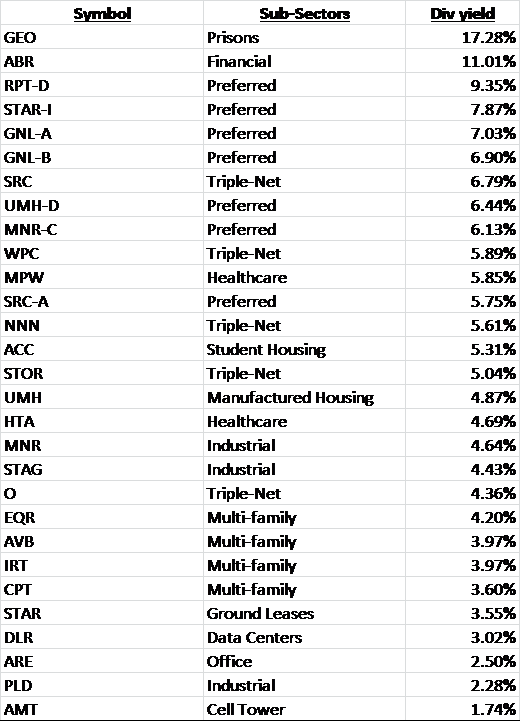

I believe the demand for high dividend stocks will increase over the next few years as we get back to a more normal environment but interest rates remain low to make sure the economy can get a more normal footing and governments like the United States can pay back or refinance their own debt at low interest rates. Therefore, REITs are well positioned to incur debt at historically low interest rates, grow, and pay solid dividends to their investors. Right now, here are the annual dividend yields my different REIT investments are paying (as of earlier this month):

These dividend yields sure beat the 10-year treasury yield of 0.6%, the average S&P dividend yield of 1.7% and many of these REIT stocks have the potential to increase 25-50% over the next few years. Do your own diligence but take a look into REITs as a possible way to have real estate generate wealth for you this time around.

Leave a Reply